|

| A good investment? |

The Tribe is currently going through a period of EXTREME spending.

First up this post is not about idiotic hedonistic spending. We have not been to Bali (ever), we do not have silly fuel guzling, flash cars, we do what we can ourselves and do not rely on expensive services. It is about:

- What have we spent money on

- A case study on good spending

- Have a play with the free FISH timeline planner

THE.FuTuRe: "I did not think they would last long in financial independence - the spending bug has finally got them"

Let's have a look at what we have spent (invested) money on and why we consider it useful in the pursuit of FISH.- We have installed a really cool eco heating system for new house:

- 25kw wood gassification boiler with a 1000 litre water buffer tank

- 300 litre solar water tank with heat exchange between the two tanks - new unpressurised design.

- 3 chimneys

- two 4kW wood burning stoves

- So much insulation we do not know what to do with it all other than double it up

- Very low running cost - minimal electricity (pumps and controllers), Purchase of wood (currently free as we are using the wood we have available around the house (~15 dead trees).

- Electricity - break even

- Wood cost of £500 per year

- Grow some of our own food and medicine

- Tools and machines: vegetation mulcher (to fertilise and protect the fruit trees), chain saw and safety equipment (we have lots of dead trees), axes, shovels, well pump (this will halve our water bill as we can water the garden and vegetable patch with free water)

- Aim is to grow our own Fruit and Vegetables in the Summer \ Autumn. Initial aim is to save 30% of our grocery shop for 6 months of the year (we currently spend £321 on food and consumables per month so saving 30%*321*6 = ~£580 per year

- Have free wood for several years

- Free water for the garden

- Our second hand 1.5 Diesel Renault Clio consumes HALF of the fuel of my 1.6l petrol WV GOLF

- Re-negotiated the insurance and BOTH cares are less than our payments on ONE CAR in the UK

- No yearly road tax in France (was £180 in the UK)

- Bi Annual Car Check (Control Technique) in France versus Yearly in the UK

- Saving 180(tax), 50(insurance) £700(Fuel), MOT £30 =£960 - Car Cost £5800 time to payback = 5800/960 = ~ 6 years

THE.FuTuRE - "What a waste of time CoNTeNDeR all that work - why bother. New technologies are making everything CHEAPER - keep with the system."

CoNTeNDeR - "It's an investment - the value of your investments may fall, blah blah blah. At least it is in my control not yours!"

How much would we need to earn each year to pay for the savings?

Consider this £2,480 having to be earned after tax. Tax at the lower rate of 20% and Social charges at 8%, you would need to earn £3,174Assuming a 5% return on investment you would need £3,174/.05 = ~ £63,500 working for you that needs to provide a return that increases at least in line with inflation.

How much have spent / invested to get the savings?

Compare that to the investments we made above to reach the same amount of "return", Car £5,800, Heating £19,000, Gardening Equipment £1,500, Insulation and shutters, £7,000 = £33,300 & we get some completely inflation proof protection with regards solar hot water, home grown food, well water and wood.Does it make sense to spend savings in this way?

- £63,000 need to be invested to pay for living costs of £2,480 (£3,174 before tax)

- £33,300 need to be spent to reduce living costs by £2,480

Consider the following case: if you had 100,000 in savings, your earned income is 25,000 per year (post tax) and you are saving 30% of your income (living costs = 25,000 - 30% = 17,500)

Case 1 - You don't spend the money

100,000 invested returns 5,000 per year at 5%

You can save 30% of a salary of 25,000 = 7,500 per year

Living cost 17,500 per year

TOTAL SAVINGS = 12,500 per year STARTING CAPITAL = 100,000

Case 2 - You spend the money

100,000 - 33,300 = 66,700 invested returns 3,335 per year at 5%

You can save 30% of a salary of 25,000 = 7,500 + the savings of 2,480 = 9,980 per year

Living cost 17,500 - 2,480 (reduction due to savings) = 15,020 per year

TOTAL SAVING = 13,315 per year STARTING CAPITAL 66,700

In this case (*see parameters) this is what your investment capital may look like in 25 years time. It takes around 19 years for the "purchases" to reach the same capital balance if you just carried on saving

*Income increases at 3% per year (25K starting point)

*Inflation increases at 4% per year

*Investments return on average 7% per year

*Living costs start at 17.5K (15K reduced living cost)

THE.FuTuRe: "19 years! to catch up and that is assuming just 7% return on invetment - aren't you just betting on your Eco system which will probably be obsolete before long! - Burn the hydrocarbons baby and smell the smoke of progress you tree hugging chimp."CoNTeNDeR - "Sure I should be one of the sheeple, go with the flow, listen to the mainstream media,indoctorateeducate the kids to be good consumers, build reliance instead of resillience, be part of the team instead of an odball fanatic hiding in a eco hideout scared to go out"MR.REaLiST - "Sounds good to me CoNTeNDeR plan ahead a bit, why sit still and wait.MR.PeSSiMiST - "What are you doing - ruining the lives of your kids - molly coddling them from the real world.MR.OPTiMiST - "Everything is awesome, chill, relax and have some fun man, thinking is so outdated. Everthing is Now Now Now and to your doorstep if you like!"

What can we learn from this case study?

- Spending is bad for very early financial independence (especially unproductive spending)

- A large starting point (inheritance) makes a massive difference

- Productive spending will pay off in the LONG term - if you need to move the investment in the house may be "lost"

You need to SAVE and BUILD capital to benefit from the power of COMPOUND INTEREST instead of SPENDING to reduce your costs for very early retirement.

You should look at ways to reduce costs through lifestyle choices. For example, choosing not to buy something or some service and live in a cheaper place.

Why did the TRiBe do it then?

Like any decision there are unique reasons and circumstances behind any decision. Arbitruary if you forego all spending it (saving and no spending) can have different outcomes. Some can be negative such as not moving (costs) for a higher paying job, failing to look after your health.In the Tribe's case the bucks have really been invested for the long term in our new life. This investment reduces our dependence on VARIBLE or DECLINING CASH FLOW, to some degree PROTECTS CAPITAL and increases our resilience \ self sustainability:

- We get to live in a mortgage-freehouse

- The house had no heating and minimal insulation so we chose an energy efficient solution.

- My old car had already done 150,000 miles - a new car was needed for reliability and backup.

- We have a degree of self sufficiency (land, water and fruit trees)

- Our net worth is not as exposed to market crashes as we now have a wider asset allocation.

Why this case doesn't make sense for Financial Independence Seeking

- House prices are at historical highs versus earnings.

- Renting can often be cheaper than buying and paying for a mortgage

- Buying a property generally means SPENDING your investment pot to INVEST in lower living costs - Think this through carefully.

- Owing a house can reduce your flexibility to move for a better job.

- A house is a liability. You have maintenance costs and property taxes.

- A larger capital investment pot can compound very fast in a bull market providing more capital to re-deploy in housing etc later.

- Cheaper heating systems (inital installation costs) are available. Personal choices such as live in only a couple of heated rooms in the winter (which is fairly short in the SW of France) would only require one 12kW stove.

- Live close to your work to avoid the car costs

|

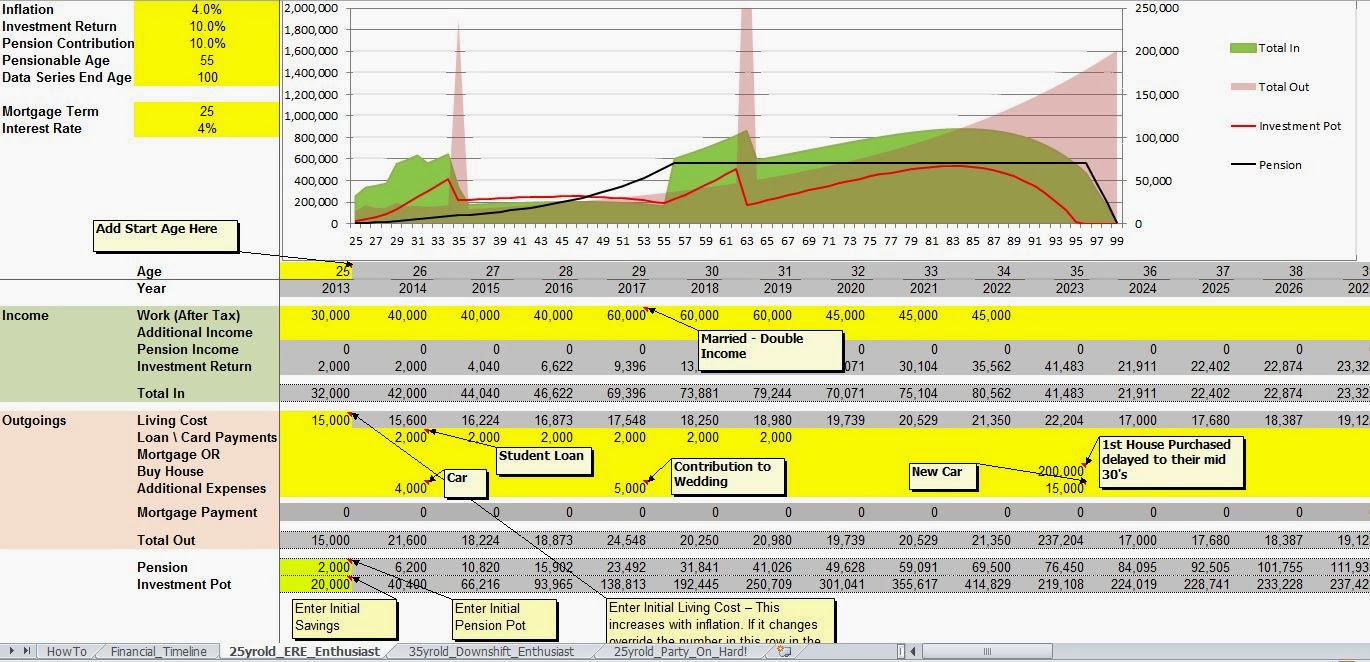

| Financial Timeline Planner (click to download excel file) |

Perhaps if we all conserve resources better we would actually have more as a society. We would leave more for the future and instead of just burning fuel (also known as money) the savings can be used to build a better world to live in.

THE.FuTuRe - "Wake up you muppet - that is NOT how we have been told the world works, don't think just do it"

THE.CoNTeNDeR - "We will just do it... our way"

Peace, prosperity and happiness

CoNTeNDeR

Welcome New Readers! Please take a look around.Click here to find out more about THE.TriBe and the blog is or perhaps browse the all posts list, Please feel free to play with the planning tools and checklists. If you liked this post can you please spare a few seconds to share it?

Post a Comment

Are you planning for financial independence and wondering what to do with it. If so is any of the content on this blog of use to you? I would appreciate any comments you have. All the best C